How Much Deposit Do You Need for a Presale in BC? Full Guide

By Alex Dunbar, REALTOR · REAL Broker BC Ltd. · Updated April 2026 · 10 min read

The typical BC pre-sale deposit is 20% of the purchase price, paid in 4 installments of 5% each over roughly 12 to 18 months, with the remaining 80% due at building completion. On a $700,000 unit that's $140,000 out-of-pocket before you ever hold the keys. This guide breaks down when each installment is due, where the money sits, and what to negotiate before you sign.

In This Guide

Every Deposit, Every Deadline, Explained

At a Glance

The BC Pre-Sale Deposit in 3 Numbers

Typical Total

5% to 20%

of purchase price

Installments

1 to 4

of 5% each

Typical Gap

3-6 months

between deposits

Numbers reflect the standard BC new-construction schedule. Individual developers vary: always confirm your specific deposit schedule in the disclosure statement before signing.

Why Deposit Structure Matters

The deposit on a BC pre-sale is the part of the purchase most buyers underestimate. A resale home typically takes a single 5% deposit at subject removal, held by your buyer's brokerage for a few weeks before completion. A pre-sale takes 20%, split over a year or more, held by the developer's lawyer until the building is finished, which can be 2 to 5 years away from the day you sign.

DOLLAR SCALE

On a $700,000 pre-sale unit, a 20% deposit is $140,000 locked up before completion. On a $900,000 townhome it is $180,000. That is 4 to 5 times the typical resale deposit sitting in trust for 18 to 36 months, with no access to the capital and modest interest credited at close.

Three realities shape every BC pre-sale deposit conversation:

- Deposits are cash, not equity: you can't finance deposit installments with your mortgage. Every dollar comes from savings, family gifts, or liquidated investments.

- Timing is front-loaded: most of the 20% is due in the first 12 months of a 24 to 36-month project. You need the cash available early, not at completion.

- Missed deposits kill the deal: a single missed installment is a contract default. You lose the unit, prior deposits, and any paper gain since signing.

The sections below walk through each installment, what to negotiate, and where the money actually sits while you wait.

The Typical BC Pre-Sale Deposit Structure

The standard 20% deposit schedule on a BC pre-sale breaks into 4 equal installments of 5% each, spread over the first 12 to 18 months after contract. The remaining 80% is mortgage-funded at completion. Here is the full schedule on a $700,000 unit for reference.

Deposit Thresholds You Should Negotiate

Most BC pre-sale contracts are presented as non-negotiable. In practice the deposit schedule is one of the few line items where developers will flex, especially in slower markets or when a project is behind its pre-sale targets. Before getting into specific levers, it helps to read what the developer actually wants from you, since the answer changes over the life of the project.

The Lever Flips: Capital Early, Price Later

Early in a launch, before the project hits the 60 to 70% pre-sale threshold that unlocks construction financing, the developer needs your capital more than they need top-of-market price. They are racing to prove demand to the lender, and the size of buyer deposits in trust feeds directly into that math. In that phase developers will often trade a discount on the unit price for a heavier deposit weighted toward the front of the schedule, say, 15% at contract instead of a 5+5+5+5% drip. On a slower launch a buyer who can wire more cash sooner can sometimes pull 2 to 5% off the list price, because the bigger early deposit moves the construction-loan pre-conditions in a way a smaller installment doesn't.

Once the construction loan is locked, the lever flips. The developer is no longer hunting capital, they are hunting margin per unit on the remaining inventory. They will often accept a smaller deposit (10 to 15% total) because cash is no longer the bottleneck, but they'll hold firm on price in a way they could not at launch. Buyers who come in late typically trade flexibility on deposit size for a tighter ask price.

Read where the project sits before you write the offer. A new launch still chasing pre-sale targets is a very different negotiation than a 90% sold-out tower with 6 holdback units. Regardless of stage, three specific levers are worth pushing on:

- Lower total deposit (15% or 10%): investor-focused towers usually hold at 20%, but end-user-focused mid-rise condos and townhomes in Surrey, Langley, and Maple Ridge sometimes accept 15%, especially on later-phase launches. A 10% total is rare but appears occasionally on slower-moving product. Lower total deposit = less cash frozen in trust for 2+ years.

- Longer gap between installments: the default schedule pushes deposits 2 and 3 close together (30 to 60 days and 6 months). Asking for 90 days and 9 months gives you time to stage liquidity. Developers typically agree to this at contract stage, rarely after.

- Capped assignment fee: not a deposit clause itself, but tied to deposit risk. If life changes and you can't fund installment 3 or 4, being able to assign the contract is your escape valve. Negotiate the assignment fee to a fixed dollar amount (e.g. $5,000) rather than a percentage or "developer's sole discretion" clause.

None of these are guaranteed. All 3 are worth asking for, particularly on any launch that has been selling for 6+ months, since those are the projects where the developer's internal sales targets create real negotiation pressure. See my Pre-Sale vs Resale in Langley breakdown for how these deposit tradeoffs compare against a standard resale offer.

Where the Money Actually Goes

Every deposit dollar on a BC pre-sale is held in trust under the Real Estate Development Marketing Act (REDMA). The developer cannot spend it on construction, marketing, or anything else until your unit closes and title transfers. That trust-account requirement is the single biggest consumer protection in BC new-construction law.

REDMA TRUST-ACCOUNT RULES

Who holds it: the developer's lawyer (or a brokerage trust, on smaller projects). Not the developer.

Can the developer use it: generally no, until completion. Limited exceptions exist if the developer posts equivalent security (a deposit protection bond) approved by the Superintendent of Real Estate.

If the project cancels: your deposit plus accrued interest is returned to you in full.

If the developer goes bankrupt: trust funds are protected from the developer's creditors by statute.

The interest earned on trust-held deposits is typically credited to the buyer at completion, though some newer contracts quietly assign it to the developer. Read the interest clause before signing: on a $140,000 deposit held for 2 years at 3 to 4%, the interest can add up to $4,000 to $7,000 at close.

The net effect: your deposits are safer in a REDMA trust account than they would be sitting with the developer, but they are also locked. You can't access them if a life event (job loss, medical, family emergency) hits during the 18 to 36-month window. Plan your cash-flow buffer accordingly.

How Lenders Approve the Construction Loan Behind Your Deposit

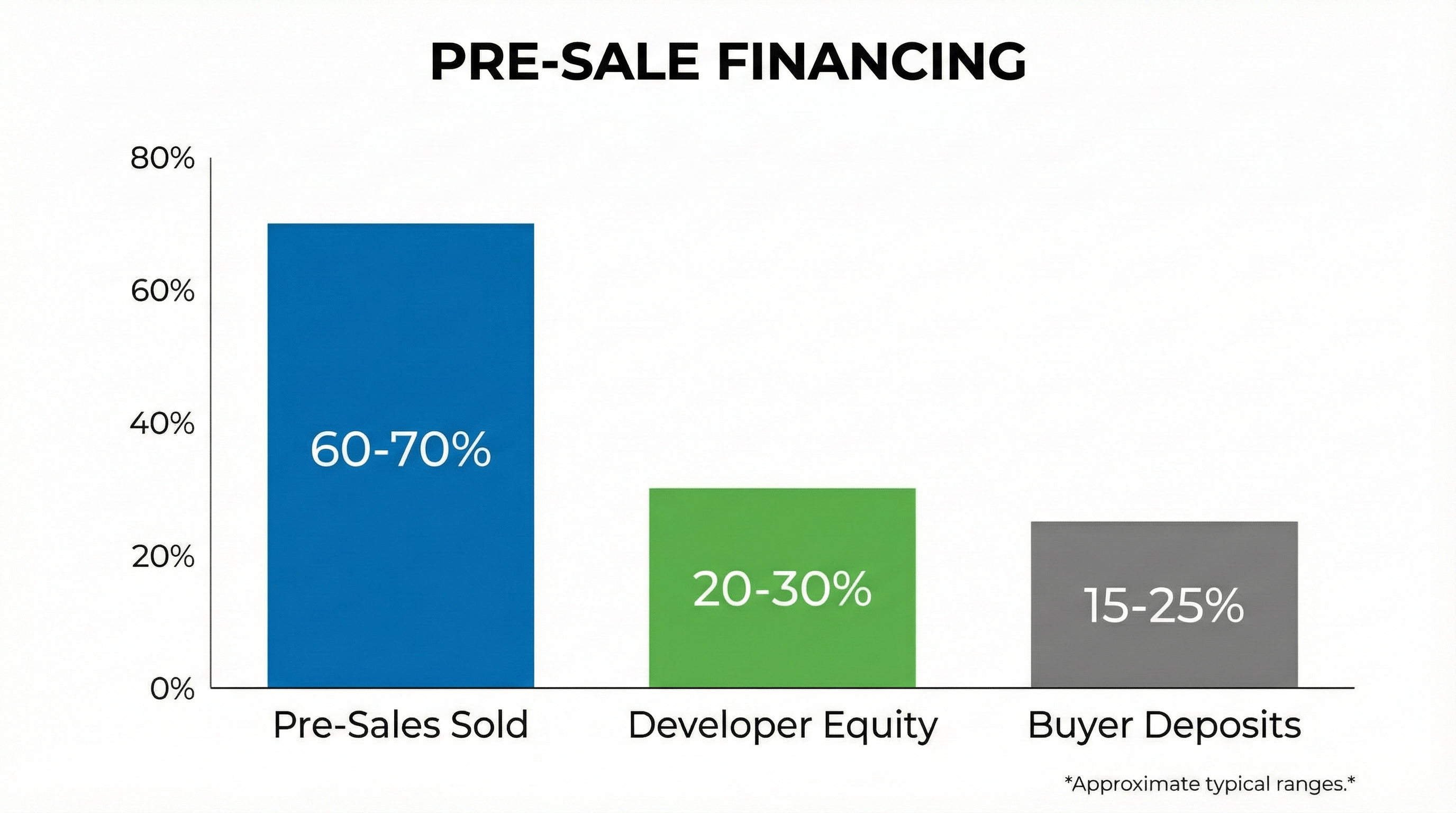

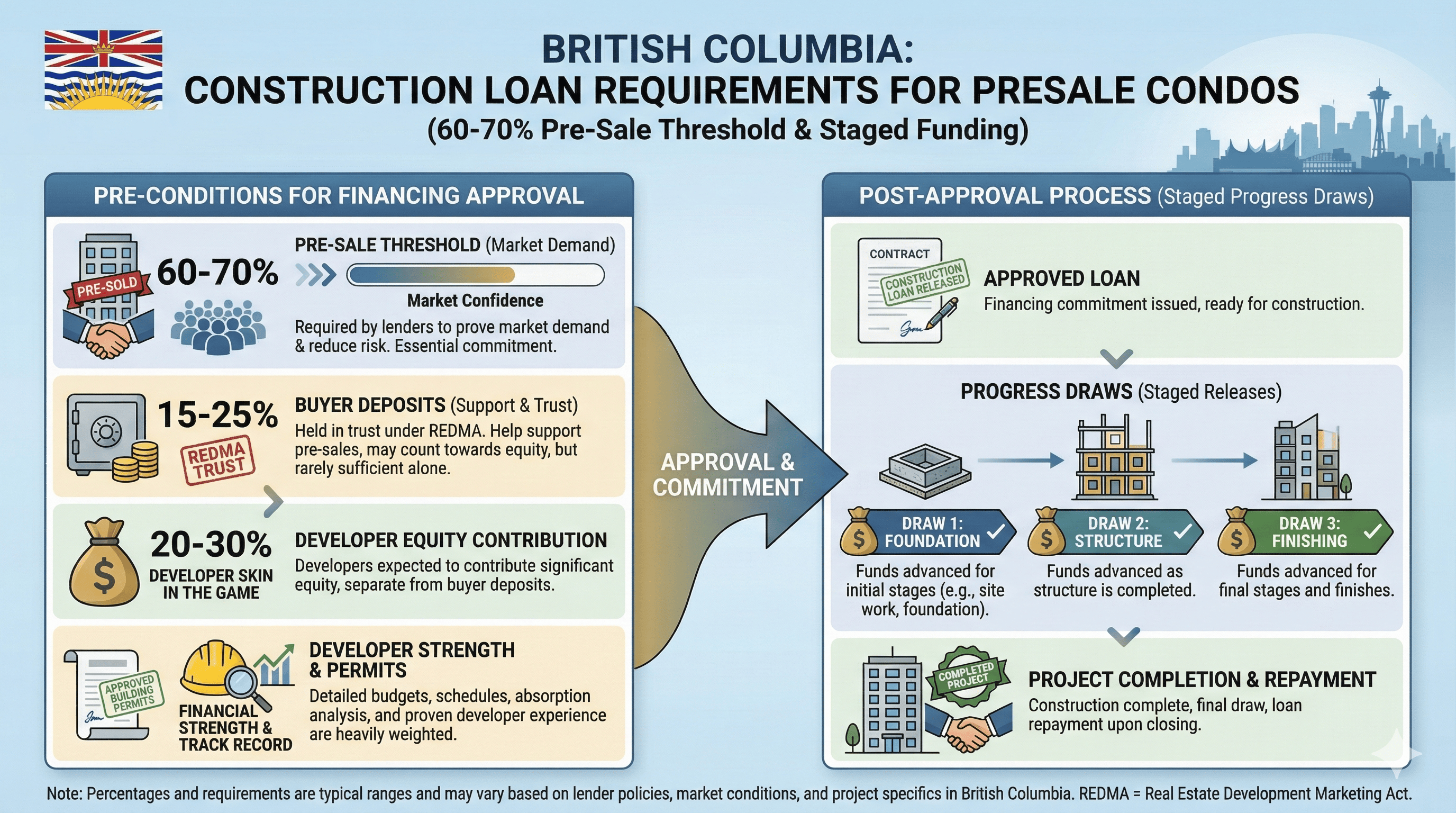

Your deposit is one of three legs holding up the project. Lenders won't release the construction loan until the developer has hit a pre-sale threshold (typically 60 to 70% of units sold), contributed their own equity (20 to 30%), and booked buyer deposits in trust (15 to 25%). The bar chart below shows the rough funding stack that gets a BC tower out of the ground.

Once those pre-conditions are satisfied, the lender issues the financing commitment and releases funds in stages tied to construction milestones: foundation, structure, finishing. Buyer deposits stay locked in REDMA trust the entire time and are only credited toward the purchase at completion. The diagram below maps the full pipeline from approval through final draw.

Common Mistakes Buyers Make

- Assuming deposit and down payment are the same thing: the deposit is front-loaded cash held in trust. The down payment is what funds your mortgage at completion. Both come out of your pocket, but on different timelines, and many buyers run out of cash between them.

- Using all their liquid savings on the deposit: depositing $140,000 across 12 months can drain your emergency fund. Keep at least 3 months of living expenses in cash outside the deposit schedule.

- Not reading the interest clause: some newer contracts assign trust-account interest to the developer. On a 2-year hold, that can be $4,000 to $7,000 you did not know you were giving up.

- Ignoring the assignment clause: if you can't fund installment 3 or 4, assignment is your escape. Contracts that prohibit assignment or charge uncapped developer-discretion fees lock you into the full 20% whether your life stays stable or not.

- Skipping the 7-day rescission review with a lawyer: BC gives you 7 days after contract to cancel without penalty. Most buyers use it to "think". A real estate lawyer can use it to flag clauses you'll regret 2 years later. Budget $400 to $700 for a proper contract review inside the window.

- Not planning for GST on top: GST (5%) is due at completion on top of the 20% deposit and 80% mortgage-funded balance. On a $700,000 unit that's another $35,000 cash at close, partially rebated if the New Home GST Rebate applies. It is not optional, and many buyers don't budget for it.

What Happens If You Can't Make a Deposit

Missing a scheduled deposit is a contract default under BC law. The consequences are serious enough that every buyer should understand them before signing, not after.

- Notice to cure: the developer issues a written notice, typically giving 5 to 10 business days to bring the account current. Interest may accrue on the overdue balance during this window.

- Termination: if the deposit isn't paid inside the cure window, the developer can terminate the contract. You lose the unit.

- Forfeited prior deposits: any deposits already paid become liquidated damages for the developer. On a 20% schedule where you paid installments 1 and 2 (10%, or $70,000 on a $700,000 unit), that money is gone.

- Lost upside: any price appreciation on the unit since your original contract date goes to the developer when they resell it. In a hot market that can be tens of thousands of dollars on top of the forfeited deposits.

- Potential damages claim: if the developer resells the unit at a lower price in a soft market, they may pursue you for the difference plus carrying costs. Rare, but legally possible.

The practical playbook if a deposit is about to be a problem:

- Call early: contact your realtor and lawyer the moment you see a cash-flow issue, not the day the deposit is due. Developers sometimes agree to 30-day extensions if approached 60+ days early.

- Explore assignment: if your contract allows it, listing the assignment before you miss a deposit is far cleaner than after. You recover most or all of your prior deposits.

- Consider a deposit loan: a handful of BC lenders offer short-term deposit financing secured against other assets. Rates are high (8 to 12%), but a short bridge beats losing $70,000.

The underlying rule: a pre-sale deposit schedule isn't something you "figure out as you go". You either have the full 20% mapped out in advance or you don't sign the contract.

Frequently Asked Questions

Can I put down less than 20% on a BC pre-sale?

Sometimes. Some BC developers accept 15% or even 10% total on smaller launches or slower-moving product. Investor-focused towers and high-demand launches usually hold firm at 20%. If the developer offers 10% deposit, read the contract carefully: you may be giving up something else (parking, storage, price protection, assignment rights) in exchange.

Do deposits earn interest while they sit in trust?

Yes, and the interest is paid to you at completion in most BC contracts. The rate is modest (prime minus a spread on the trust account), and on a $140,000 deposit held for 2 years you might see $4,000 to $7,000 in interest credited at close. Confirm the interest clause exists in your contract before signing: some newer contracts quietly assign it to the developer.

What happens to my deposit if the developer cancels the project?

Under REDMA, deposits are held in a lawyer's or developer's trust account separately from the developer's operating funds. If the project cancels, your deposit plus any accrued interest is returned to you. This has happened on multiple cancelled BC projects in the last 5 years (including several Metro Vancouver towers). You get your money back, but you lose the time value of it and any price lift you would have captured.

Is the deposit refundable if I change my mind?

Only inside the 7-day rescission window that BC law provides after contract signing. After day 7, your initial deposit is generally non-refundable. Exceptions exist for developer-side defaults (material misrepresentation, undisclosed changes to the disclosure statement), but those require legal review and are not easy wins.

Can I use my RRSP Home Buyers' Plan for a pre-sale deposit?

Not directly. The RRSP HBP withdrawal is tied to taking title on a home within a specific CRA window, and pre-sale deposits are paid years before completion. You can use your HBP funds at completion toward your down payment, but you cannot use them for the pre-sale deposit stages. Plan deposit cash separately.

What if I can't come up with the next deposit installment on time?

Missing a scheduled deposit is a contract default. The developer can issue a notice to cure (usually 5 to 10 business days), and if unresolved, can terminate the contract and retain prior deposits as liquidated damages. You also lose the unit, any price lift since signing, and any accrued deposit interest. Contact your realtor and lawyer the moment you see a cash-flow problem, there are sometimes workarounds (extension, partial assignment) if the developer is approached early.

How is a pre-sale deposit different from a resale deposit?

A resale deposit is typically 5% of purchase price, paid in one tranche within 24 hours of subject removal, and held by your buyer's brokerage (not the seller). A pre-sale deposit is typically 20% total, paid in 3 to 4 tranches over 12 to 18 months, held by the developer's lawyer in a REDMA trust account. The dollar scale is 4 to 5 times larger and the commitment window is much longer.

Can I assign my pre-sale contract to someone else to avoid the remaining deposits?

Sometimes, if your contract permits assignment (many newer BC pre-sale contracts restrict or prohibit it). Assignment transfers your remaining obligations to the new buyer, who takes over the remaining deposit schedule and the completion mortgage. Assignment fees to the developer run $5,000 to $25,000 on most BC projects, and any assignment profit above your original price may be subject to GST and income tax. Talk to your lawyer before listing an assignment.

Thinking About a Pre-Sale?

I'll map your deposit schedule with you before you sign.

I've walked dozens of BC buyers through the deposit schedule, GST math, and completion-day cash flow on new-construction purchases. Book a 15-minute call and we'll check the numbers against your savings, or grab my free Buyer's or Seller's Guide below.

Related Posts

Alex Dunbar Personal Real Estate Corporation

REAL Broker BC Ltd. | Living in the Lower Mainland

I help BC buyers run the deposit math, GST math, and completion-day cash flow on new-construction purchases before they sign. If you are looking at a pre-sale in Surrey, Langley, or Maple Ridge, I can walk the contract with you inside the 7-day rescission window.

Featured Guides

BC pre-sale contracts and REDMA rules change. Verify current deposit structures, trust-account provisions, and assignment clauses with your realtor and lawyer before signing any contract. This article is for informational purposes only and does not constitute financial, legal, or investment advice.

Categories

Recent Posts

GET MORE INFORMATION